The End of Cheap Money and the Beginning of a New Growth Model

Mongolia has graduated. But hasn't realized it yet.

For two decades, we borrowed the world's cheapest money. The IDA window opened in 1991, and capital flowed in at zero percent interest, sometimes with thirty-year tenors. We built schools. We paved roads. We electrified gers. We did all of this on terms no commercial bank would have offered, because no commercial bank was supposed to. That era is over. As of 2021, Mongolia is largely an IBRD borrower. The interest rate has teeth now. Every project has to clear a real hurdle: can it actually pay back what it costs?

This is not a small administrative shift but a fundamental change in how a country has to think about its economy.

And it is not just Mongolia. The same underlying shift is affecting every middle-income economy in Asia at roughly the same time. The question we should be asking ourselves, urgently, is not “how do we keep the cheap money coming?” The cheap money is gone. The question is who, exactly, is supposed to drive growth now.

The world that built us is gone

Look at how much has changed in a single working lifetime.

In 2000, the Asia and Pacific region produced about a quarter of global GDP. Today, the region's share sits closer to 47 percent. GDP per capita has risen from roughly $4,200 to $23,230. Extreme poverty across Asia/Pacific has fallen from 21 percent to about 3 percent. Whatever else you want to say about the last quarter century, this is the fastest mass exit from deprivation in human history.

The development banks were part of that story. The World Bank, ADB, AIIB, EBRD, and the bilateral agencies wrote the playbook for getting people out of poverty, and the playbook worked. The uncomfortable truth is that doing it well puts them out of the old job.

The new questions are not the same as the old ones.

The old question was: how do we move 21 percent of our people out of extreme poverty? The new question is: how do we close the inequality gap that opened up while we did it?

The old question was: how do we get every child reading? The new question is: how do we get every graduate coding, designing, building?

The old question was: how do we connect a city to the grid? The new question is: how do we make that grid reliable, clean, and competitive enough for a data center, an EV plant, or a smelter that runs at international tariffs?

You cannot answer the second list with the first list's tools. And the first list's tool was, fundamentally, a government with a cheap loan.

Why the government is not the right operator anymore

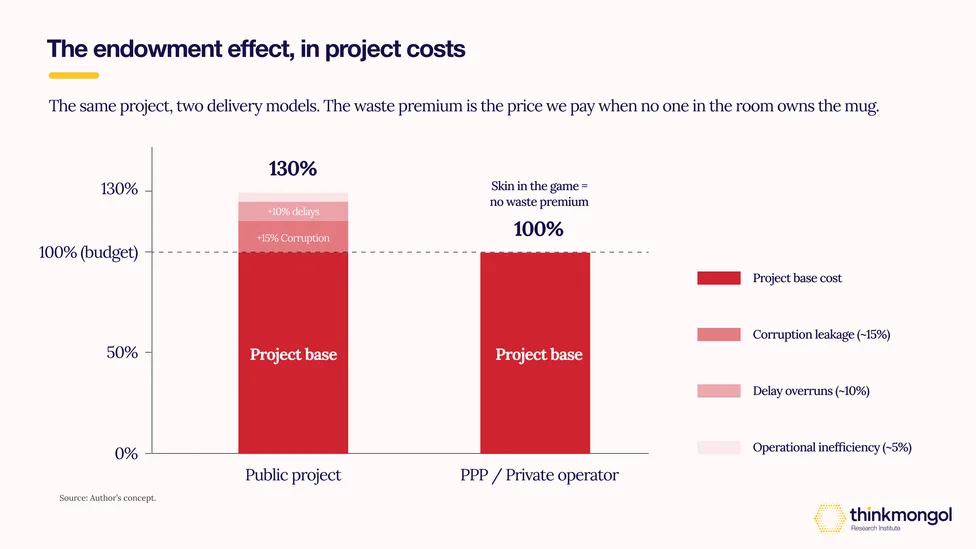

Here is the result from a famous experiment. A coffee mug costs $2.87 when it is not yours. The same mug, once you own it, jumps to $7.12. People simply treat their own things differently. They protect them. They maintain them. They fight for them.

This is the endowment effect. It is also, frankly, why public projects so often disappoint.

It is not that public servants are worse people than private ones. The issue is that nobody on a typical government project has personal money on the line. If the road takes three years instead of one, the contractor still gets paid. If the procurement is steered, the politician gets re-elected anyway. If the maintenance is skipped, the deficit absorbs it. The project is no one's “mug.”

Run the numbers. A typical public project in Mongolia ends up costing roughly 130 percent of its initial budget once corruption, delays, and ordinary inefficiency are loaded in. Estimate it modestly: 15 percent in corruption-related leakage, 10 percent in delay overruns, 5 percent in plain operational inefficiency. The same project, structured as a public-private partnership with a private operator who carries the construction risk and the operating risk, comes in at around 100 percent of budget. This is not because the private operator is virtuous, but rather because the lender is auditing every drawdown. Because the equity holder loses real money if the project slips. Because the operations team gets bonused on uptime.

That is the difference between renting and owning. That is skin in the game.

I have lived this. Mongolia's second grid-connected battery storage system was delivered in six months from concept to commissioning. Six months. Through a PPP model, with private equity carrying the risk and a sub-sovereign bond financing it. Had the same project been pushed through as a sovereign-funded build, the approval cycle alone would have taken years despite the same engineering, same site, and the same suppliers. The difference, however, was who was on the hook if it slipped.

Mongolia's specific squeeze

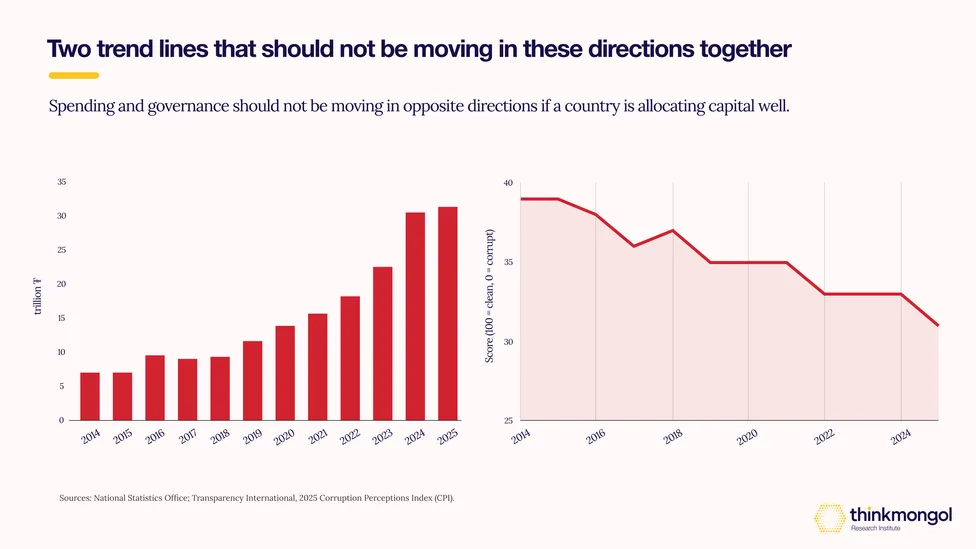

This is not theoretical. Two trend lines are crossing in Mongolia in a way nobody should be ignoring.

First, the government's budget keeps growing. Total nominal expenditure has gone roughly vertical since 2014. Real expenditure has expanded too, even after inflation. The gap is what economists call a real expansion of the state.

Second, our Corruption Perceptions Index (CPI) ranking has been declining year after year.

A growing state and a worsening governance score are a dangerous combination. Every additional tugrik flowing through a public procurement system that cannot reliably reward the best bidder is a tugrik earning less than it could have. Multiply this across a decade of mining-driven revenues and you start to see why headline GDP can rise while household welfare stalls.

This is the part most policy debates miss. Private sector development is not an ideological argument, but an economic one grounded in arithmetic. We cannot keep growing the productive economy by routing more and more national savings through institutions that have been getting demonstrably worse at allocating capital.

The MDBs already pivoted. The question is whether we will

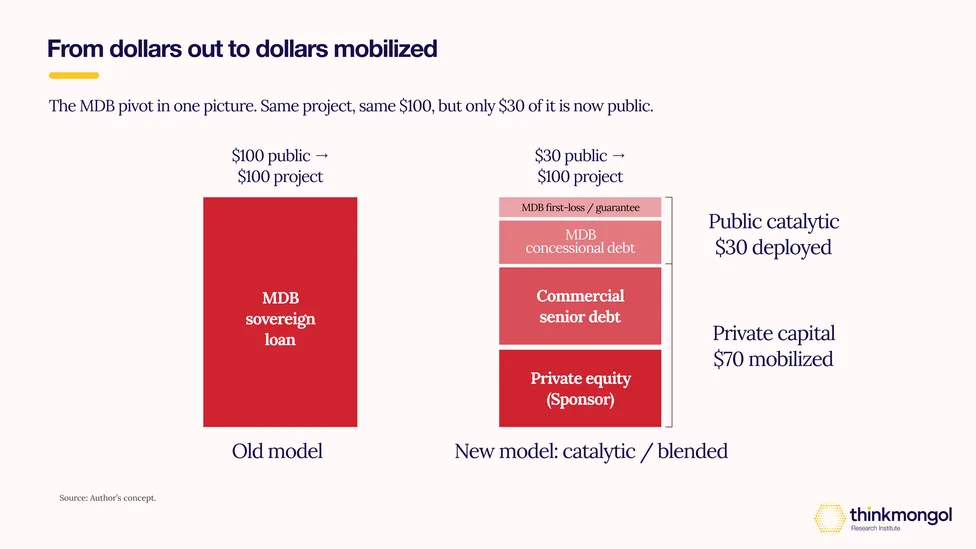

Here is what people inside the system know but rarely say out loud. The development banks have been quietly rewriting their own playbooks for the better part of a decade.

The old model was simple. A sovereign borrows. The bank disburses. The country builds. Headline metric: dollars out the door.

The new model is harder. The bank takes the first-loss tranche. Or guarantees a slice of the political risk. Or anchors a fund that pulls in commercial pension money behind it. Headline metric: dollars mobilized per dollar of public capital deployed. The ratio matters more than the absolute number.

The ASEAN Catalytic Green Finance Facility (ACGF) is the most visible example. It blends concessional capital from MDBs and donors with commercial finance to make green infrastructure projects bankable across Southeast Asia. The whole point is not to fund any individual project. It is to make the project investable for everyone else.

This is what “de-risking” actually means. It does not remove risk from the world. It allocates risk to whoever can carry it most cheaply. Political risk to the MDB. Construction risk to the contractor. Demand risk to the offtaker. Equity risk to the developer. When risk sits in the right pocket, capital flows. When it sits in the wrong pocket, the project never closes. That is most of project finance, in one sentence.

The only way forward is through transition from government led to private sector led growth (via PPP) and enabling a favorable ecosystem for businesses. Private consumption and investment remain the primary drivers of growth in resilient economies.

The MDBs cannot do that work for us. They can only meet us halfway.

So what does the government's new job actually look like?

Three things, mostly.

Speed. Permitting that takes 18 months for a wind farm in a country with the world's best wind resources is not regulation. It is sabotage by paperwork. A solar project in the United Arab Emirates can move from license to financial close in under a year. The same project in many of our neighbors takes three or four. The wind in Mongolia is the same wind. The sunlight is the same sunlight. The difference in deployment is purely institutional.

The new PPP Law, in force since December 2023, was meant to fix this. It replaced the 2010 Concession Law explicitly because of certain documented failures, including the illegal selection of participants, the absence of clear procedural guidelines, and a lack of administrative oversight through the selection, contracting, and implementation phases. On paper, the upgrade is real. A PPP Center under the Ministry of Economy and Development manages the pipeline. Templates and tender documents have been standardized. The 2023 Regulation on Government Support and Guarantees introduced obligation and payment guarantees that, in principle, give lenders recourse if the state breaches its commitments.

The gap is between paper and practice. A private initiator still has to fund its own feasibility study, then wait for Cabinet endorsement, then wait for the ministry to organize a tender, then bid against itself for the project it originated. Each step lives in a different agency. Each agency has its own review clock. The Asian Development Bank's 2025 Country Partnership Strategy is direct about it: “capacity constraints and a weak project pipeline continue to limit private sector engagement in infrastructure.” If a wind farm takes 18 months to permit in a country with 2,600 GW of renewable potential, the law on the books is not the binding constraint. The administrative path through that law is.

Predictability. Investors price uncertainty. If the rules can change between the licensing stage and the operating stage, the cost of capital goes up sometimes by hundreds of basis points. If your wind farm's PPA allows for curtailment, meaning the national dispatch center can refuse to purchase your power whenever they want without recourse, then your PPA is not bankable (not worth the paper it's printed on) and your financial projection is not credible. That cost lands in the tariff that ordinary citizens eventually pay for power, water, transport, and telecommunications. Stable, transparent rules, and strong reliable contracts are not a giveaway to the private sector. They are a discount on what households pay later.

Quality of entrants. The standard advice here is to demand more competition. Mongolia does not actually suffer from too few people wanting to bid. We suffer from too many bidders who show up without the equity, the technical capacity, or the balance sheet to carry the project they are bidding for. The first reform the procurement system needs is a real prequalification regime. Demonstrable upfront capital. Audited track record. Performance guarantees that bite. Not paperwork that looks like prequalification and in practice waves anyone through.

Fair terms. The other half of the same problem sits on the government's side. A PPP only attracts serious capital if the terms are worth bidding on. If the state insists on keeping a majority equity stake in every project, reserving the right to terminate without compensation, controlling tariff-setting after financial close, and retaining veto rights over operational decisions, the only entities willing to sign are the ones who plan to make their money before commissioning rather than after. Real private capital prices that risk and walks. To attract the partners we actually want, the government has to be willing to concede genuine control: equity, decision rights, tariff certainty, and contract sanctity. This should not be thought of as a gift to the private sector, but rather the price of a credible PPP.

What happens if we miss this transition

Countries that miss this shift do not stagnate. They regress.

Argentina ran the experiment in slow motion for half a century. Sri Lanka ran it faster, and ended up in sovereign default in 2022. Lebanon ran it through a different mechanism, with exclusive distribution agencies that turned the import economy into a system of legalized monopoly rents, and then through a banking sector collapse that wiped out a generation of household savings.

The common thread is not corruption alone, although that is part of it. It is governments that kept trying to be the operator instead of the enabler. Governments that ran airlines and lost money. Governments that subsidized fuel until the budget broke. Governments that printed currency to plug the gap. Governments that regulated entry to protect incumbents and called it development policy.

Mongolia is not yet on that path. But we are not as far from it as we would like to think. A 12 percent policy rate is not the symptom of a healthy economy. A growing fiscal footprint paired with a falling governance score is not a soft landing. The transition window for shifting to a private-led, MDB-catalyzed, ecosystem-enabled growth model is open right now. Windows close.

What I would ask any policymaker reading this

A few practical things.

Stop treating public-private partnerships as a financing trick to keep debt off the sovereign balance sheet. They are not that. A real PPP is a risk-allocation framework. Build one, and use it.

Treat the MDBs as partners, not as ATMs. The Asian Development Bank, the World Bank, the EBRD, the EIB, the AIIB, every one of them is looking for projects that mobilize private capital. Bring them a bankable pipeline and they will bring you blended finance. Bring them a wishlist and you will eventually get a polite no.

Fix permitting and reliability before fixing tariffs. Most of what kills private investment in Mongolia is not the headline tax rate or the rate of return. It is the ugly precedent and evident risk that the government can renege on their word, will nationalize your project, and operate in bad faith.

Build the financial plumbing. Sub-sovereign bonds. Project finance bond markets. Local-currency hedging. None of this is glamorous. All of it is essential. Mongolia's first OTC municipal bond, the USD 87.2 million sub-sovereign instrument fully subscribed by IFC, took eighteen months of investor-grade documentation to put together. The next one should take six. The one after that, three. That is what institutional capacity looks like when it is built deliberately.

And finally, accept that the government's seat at the table changes. Less operator. More convener. Less regulator. More host. Less owner. More referee.

That is not a smaller role. It is a different one. Whether we play it well will decide what the next decade in Mongolia, and frankly across most of emerging Asia, actually feels like for the people living through it.

The cheap money is gone. The skin in the game has to come from somewhere else.

It is time to allow private companies to take ownership of the development of their country.

Any views, opinions, and conclusions expressed in this article are solely those of the author(s) and do not represent the official position of Think Mongol Institute.

Related Publications