Food Price Inflation, Consumer Debt, and the Vicious Cycle of Unproductive Lending in Mongolia

Mongolia’s economic story is usually told through copper, coal, and growth. That story is real, but it is incomplete. Beneath it sits another economy, more intimate and more punishing, in which households are increasingly borrowing not to invest, not to build businesses, but simply to eat.

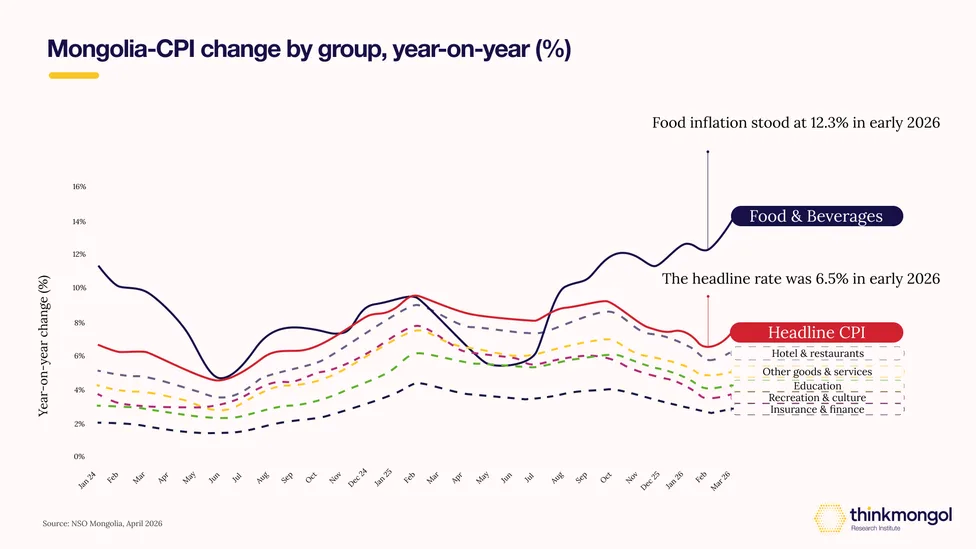

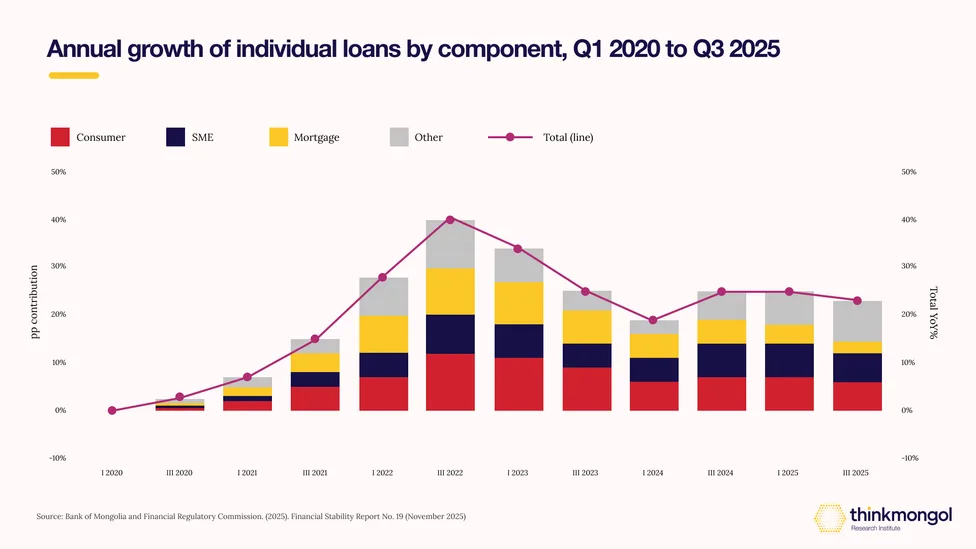

By end-2024, outstanding consumer loans in the banking system had reached the equivalent of 3.2 billion USD, a 35.5% jump in a single year. Total individual loan balances across all financial institutions reached 36.9 trillion MNT by Q3 2025. At the same time, food inflation stood at 12.3% in early 2026, nearly double the headline rate of 6.5%. The prices that matter most to households are rising far faster than the headline number suggests.

This matters because food is not discretionary: a family can postpone buying a television, but it cannot postpone dinner, and when the price of meat, flour, cooking oil, and vegetables rises faster than wages, that gap has to be financed somehow. In Mongolia, that bridge is increasingly built with high-interest consumer debt.

That is the core argument of this article: structural food inflation is pushing households into consumer borrowing, and that borrowing, because it finances consumption without simultaneously increasing output, creates a negative inflationary feedback loop. Food inflation drives borrowing; borrowing sustains demand without expanding productive capacity; prices remain high; households borrow again.

In other words, rational households are increasingly facing impossible arithmetic.

Why Food Prices Keep Rising

Food inflation is embedded in the structure of the Mongolian economy. Mongolia is fully import-dependent for rice, sugar, and cooking oil, roughly half reliant on flour, and grows fresh vegetables domestically for only four months of the year. Everything else comes through two border crossings, one with China, one with Russia. When either closes, shelves quickly empty. To make matters worse, the tugrik has lost nearly 45% of its value against the dollar over the past decade, so every import costs more in local currency every year.

In spring 2026, wholesale beef at Ulaanbaatar’s Khuchit Shonkhor market had climbed to MNT 27,000–32,000 per kilogram, while mutton rose 45% in twelve months. As one vendor put it: “When prices are expected to fall in summer, they only drop 100–500 tugriks. When they rise, they jump 3,000–4,000.” That asymmetry reflects concentrated distribution power at every step from herder to consumer, with each stage adding its own margin before the meat reaches retail shelves.

Engel’s Law holds in aggregate: the average household spent about 18.4% of total expenditure on food in 2025. But averages conceal the real pressure – lower-income households comparatively spend far more of their budgets on food, meaning food price hikes hits them disproportionally harder. Real wage growth slowed to just 2.1% by mid-2025 while household spending grew 14.7%, outpacing income. That gap is not being closed by savings but rather by loans.

The Lending Machine

Consumer loans surged 35.5% in 2024 alone. By Q3 2025, individuals held more than 60% of all bank loans. Pension loans, borrowing against future retirement income, surged 42% year-on-year after the government reversed its own restrictions under parliamentary pressure.

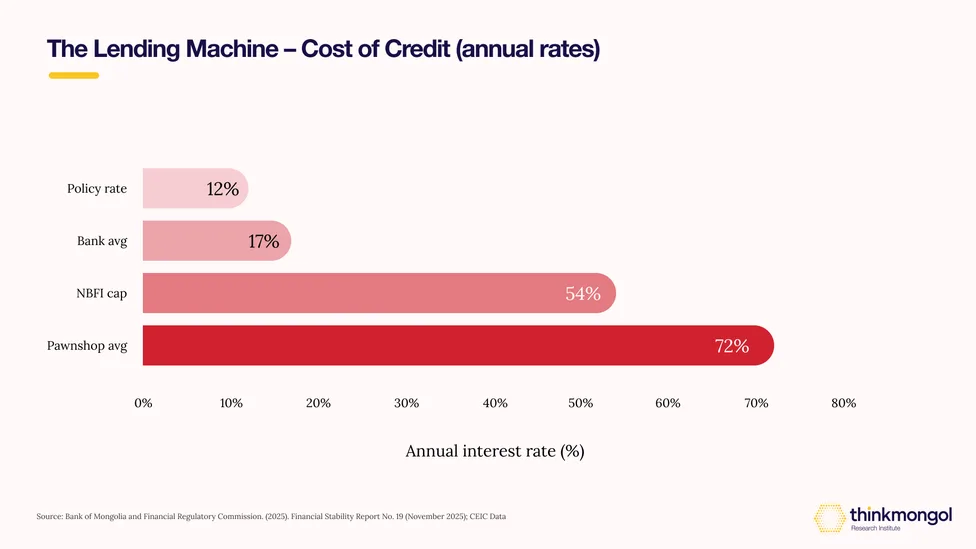

The rates are brutal. Bank lending averages around 17% annually. Beyond banks, over 570 non-bank financial institutions (NBFIs) operate in Mongolia, mostly in lending. The regulator capped NBFI consumer rates at 4.5% per month or about 54% annually. Pawnshops run at 72% a year, while informal lenders charge 1% per day: 365% annually. When the legal ceiling is 54%, the informal market charges 365%. This is the landscape distressed households navigate, and for many there is no other option.

The digital layer has widened the funnel. LendMN has 1.3 million registered users in a country of 3.5 million, one in three Mongolians have a lending app on their phone. Credit is no longer accessed occasionally through a bank branch. It sits in the pocket, always one tap away.

The distress is already visible: among pensioners, more than half have outstanding loans with average debt-to-income ratios of 84.7%. The Bank of Mongolia found that 87.7% of pension borrowers, nearly 250,000 people, have post-repayment income below subsistence levels. For 40,500 of them, the entire pension goes to loan repayments.

Nothing is left. There are an estimated 2.8 million NBFI borrowers in a country with roughly 2.4 million adults: multiple loans are the norm, not the exception.

Why Borrowing to Eat Makes Prices Worse

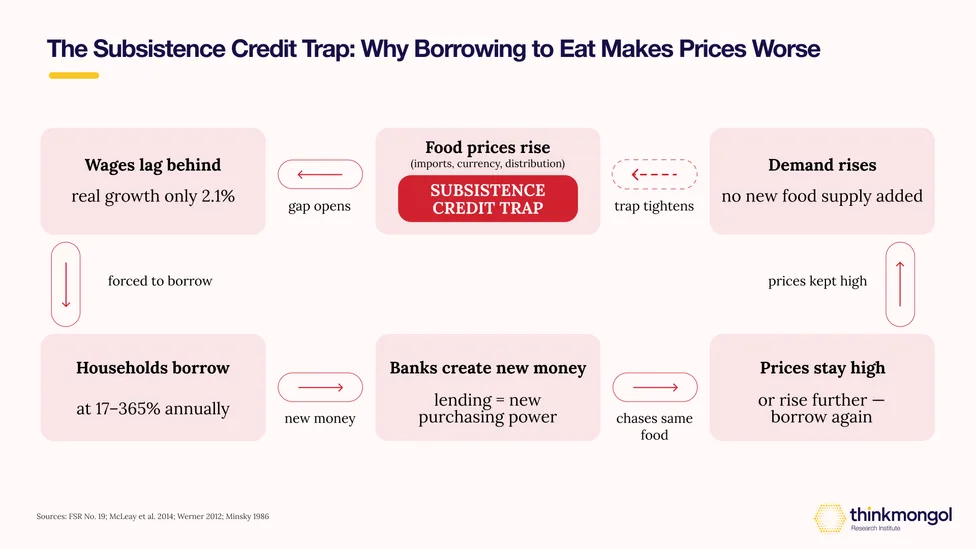

The mechanism is counterintuitive but well-established. When a bank lends it creates ‘new money’ by issuing loans without needing an equivalent amount of deposits on hand.

Every new consumer loan increases consumer demand in the economy. If that credit finances productive activities such as a factory, new output eventually follows and matches the increase in demand, thereby containing price increases. However, if loans finance food purchases in a supply-constrained market, more money chases the same amount of beef and rice. Prices stay high or rise further.

Cross-country data from 45 countries confirms it: enterprise lending raises growth and reduces inequality; household consumption lending does neither. When 60%+ of Mongolia’s bank lending flows to individuals rather than businesses, the credit system is adding fuel to inflation rather than building the capacity that would eventually ease it.

Minsky’s framework sharpens the point. Debt looks manageable at first (hedge finance). Prices rise, real incomes weaken, and households begin rolling loans to cover yesterday's obligations (speculative finance). Eventually they borrow just to repay existing debt (Ponzi finance). In Mongolia, this spiral is not driven by speculation or euphoria. It is driven by the cost of dinner. The Bank of Mongolia’s own data shows borrowers routinely restructure loans before finishing repayment. Research confirms that necessity-driven debt of this kind predicts lower growth and higher unemployment in the medium run.

The Same Story, Told Elsewhere

Turkey: food inflation hit 103% in 2022; grocery credit card purchases surged 137%. South Africa: unsecured lending grew 260% in three years; over 42% of credit-active adults are now credit-impaired. Kenya: 8 million digital loan users, 14 million accounts flagged for default, 800,000 borrowers caught loan-stacking, taking one app loan to repay another. India’s Andhra Pradesh: when microfinance institutions hit 80% annual growth and multiple lenders crowded the same distressed households, over 200 people in debt spirals committed suicide. When authorities shut the lenders down, informal rates jumped six times higher, proving the demand for survival credit is inelastic. You cannot cap it away.

The pattern is the same everywhere: food prices spike, wages stagnate, households borrow to eat, debt accumulates, and the next shock hits a more fragile base. Mongolia is not an exception, it is a particularly clear case study.

The Rational Trap

A median Mongolian household earns 2,817,600 MNT a month in nominal terms, the figure Mongolians actually see in their bank accounts. Food accounts for MNT 526,100 of that expenditure. Meat alone costs 163,536 MNT, up 15.2% from a year ago and still rising. If mutton, a Mongolian household staple, jumps a further 45%, food costs spike by another 73,591 MNT per month. The deficit doubles to 112,000 MNT. There is no buffer.

The only option is a loan. The average indebted household already repays 1,217,400 MNT a month, nearly 43% of its entire income, in loan repayments. Borrowing to cover the food gap does not solve the problem. It adds a repayment obligation on top of a deficit that already existed.

Ethnographic research documents what this looks like on the ground. Herder families take fall loans for school tuition, winter loans for food and fuel, spring loans for livestock feed after a dzud (a severe winter climatic event that causes large scale livestock death).

The cycle never breaks because the next season always comes. In urban ger districts, customers run tabs at bakeries because their entire cash income goes to bank repayments. Mongolia’s government acknowledged this explicitly: Children’s Money.

Program grants were legally restricted from being used to repay loans, because without that restriction, every transfer would disappear into debt servicing.

Nearly 30% of Mongolian children under 14 live in poverty. When a pension leaves 15 cents on the dollar after repayments, the trade-off is not between comfort and frugality. It is between eating and defaulting.

What Would Actually Help

Interest rate caps are the instinctive policy response. They are usually the wrong one. Kenya’s 2016–2019 cap collapsed credit growth from 25% to 2.4% and drove low-income borrowers toward the digital lenders the cap was meant to constrain. The problem is not the price of credit. It is the conditions that make distress borrowing rational.

Four interventions address the actual problem:

Create a legal exit from unserviceable debt. Mongolia’s 1997 Bankruptcy Law covers businesses only. A draft personal insolvency law has sat unenacted since 2019. Kazakhstan’s 2022 reform, court-supervised restructuring, simplified discharge, is a possible model.

Fix the food supply, not just the price. Greenhouse investment, cold chain infrastructure, and competition policy targeting concentrated wholesale distribution would structurally reduce the prices that make borrowing sustainable.

Redirect credit toward production. Differentiated reserve requirements, making business loans more competitive than consumption loans would shift incentives without banning anything.

Regulate digital lending properly. Genuine affordability verification, concurrent loan limits through credit bureau integration, and ending the use of pension and salary assignments as collateral for consumption loans.

The Trap Tightens with Every Payment

Mongolia’s official indicators look reasonable: GDP grew 4.9% in 2024, headline inflation is 9%, credit is expanding. But beneath those aggregates sits an economy where food inflation runs at double the headline rate, where the majority of pensioners carry loans they cannot repay, and where a large percentage of adults owe money to lenders.

The people borrowing to eat are not the problem. They are the clearest signal that the system, as currently organized, is failing them. Mongolia has to reduce the structural causes of food inflation, redirect credit toward productive activity, and give genuinely insolvent households a legal way out. If food inflation stays structurally high and consumer credit remains the main coping tool, Mongolia will keep mistaking debt-fueled survival for stability.

The trap tightens with every payment. The question is whether policy can move faster than the debt.

Any views, opinions, and conclusions expressed in this article are solely those of the author(s) and do not represent the official position of Think Mongol Institute.

Related Publications